Investing Basics

1 Book Topics

- Compounding: interest earning interest; does the heavy lifting over long horizons; Rule of 72 — years to double ≈ 72 ÷ annual return %

- Risk vs. return: higher expected return = higher volatility; choose a level you can stick with through downturns

- Diversification: don’t bet on one company, sector, or country; broad index funds make diversification nearly free (Bogle)

- Real vs. nominal return: inflation silently erodes purchasing power; always think in real (inflation-adjusted) terms

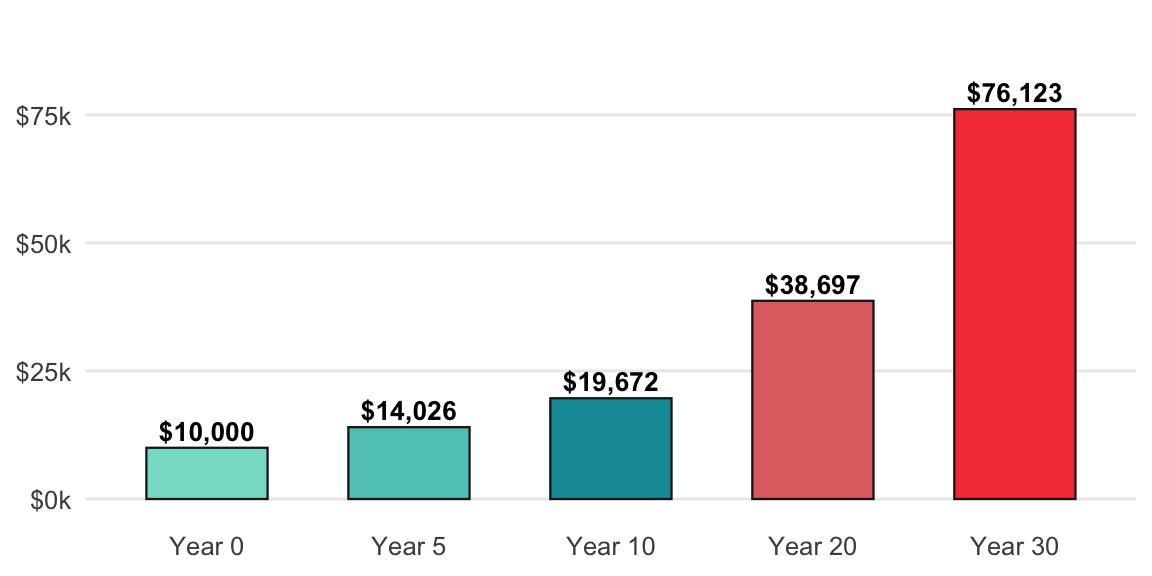

2 Future Value (Compounding)

A single lump sum growing at a constant rate.

Formula: FV = PV × (1 + r)^n

show/hide

future_value <- function(present_value, rate, years) {

present_value * (1 + rate)^years

}

rule_of_72 <- function(annual_return_pct) {

72 / annual_return_pct

}

future_value(present_value = 10000, rate = 0.07, years = 10)

#> [1] 19671.51

rule_of_72(annual_return_pct = 7)

#> [1] 10.28571

# vectorized across multiple horizons

data.frame(

years = c(5, 10, 20, 30),

value = future_value(10000, 0.07, c(5, 10, 20, 30))

)

#> # A tibble: 4 × 2

#> years value

#> <dbl> <dbl>

#> 1 5 14026.

#> 2 10 19672.

#> 3 20 38697.

#> 4 30 76123.show/hide

import numpy as np

def future_value(present_value, rate, years):

return present_value * (1 + rate) ** years

def rule_of_72(annual_return_pct):

return 72 / annual_return_pct

print(future_value(present_value=10000, rate=0.07, years=10))

#> 19671.513572895663

print(rule_of_72(annual_return_pct=7))

#> 10.285714285714286

horizons = np.array([5, 10, 20, 30])

future_value(present_value=10000, rate=0.07, years=horizons)

#> array([14025.517307 , 19671.5135729 , 38696.84462486, 76122.55042662])With present value in A2, rate in B2, years in C2:

=A2*(1+B2)^C2Rule of 72 (rate as a percent in A2):

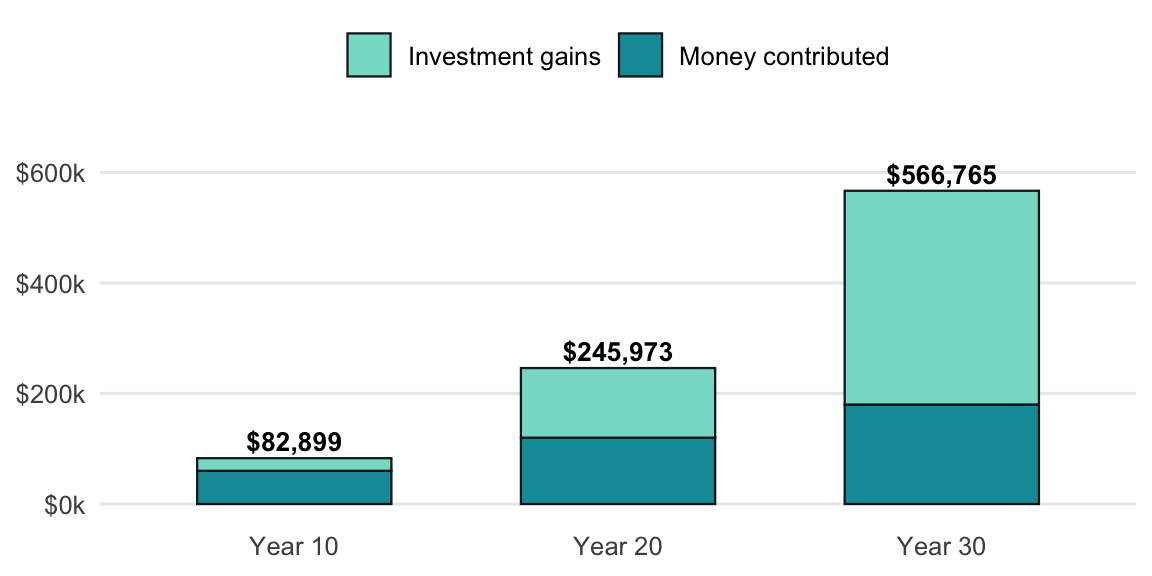

=72/A23 Future Value of Regular Contributions

Monthly investing builds wealth two ways: the money contributed and the returns on all prior contributions.

Formula: FV = PMT × [((1 + r)^n − 1) ÷ r]

show/hide

future_value_series <- function(contribution, rate, periods) {

contribution * (((1 + rate)^periods - 1) / rate)

}

# $500/month for 30 years at 7% annual (monthly rate = 0.07/12)

future_value_series(contribution = 500, rate = 0.07 / 12, periods = 30 * 12)

#> [1] 609985.5show/hide

def future_value_series(contribution, rate, periods):

return contribution * (((1 + rate) ** periods - 1) / rate)

future_value_series(contribution=500, rate=0.07 / 12, periods=30 * 12)

#> 609985.4978879723Use the built-in FV() function: FV(rate, nper, pmt)

rate: monthly =7%/12nper: months =30*12pmt: monthly contribution as negative =-500

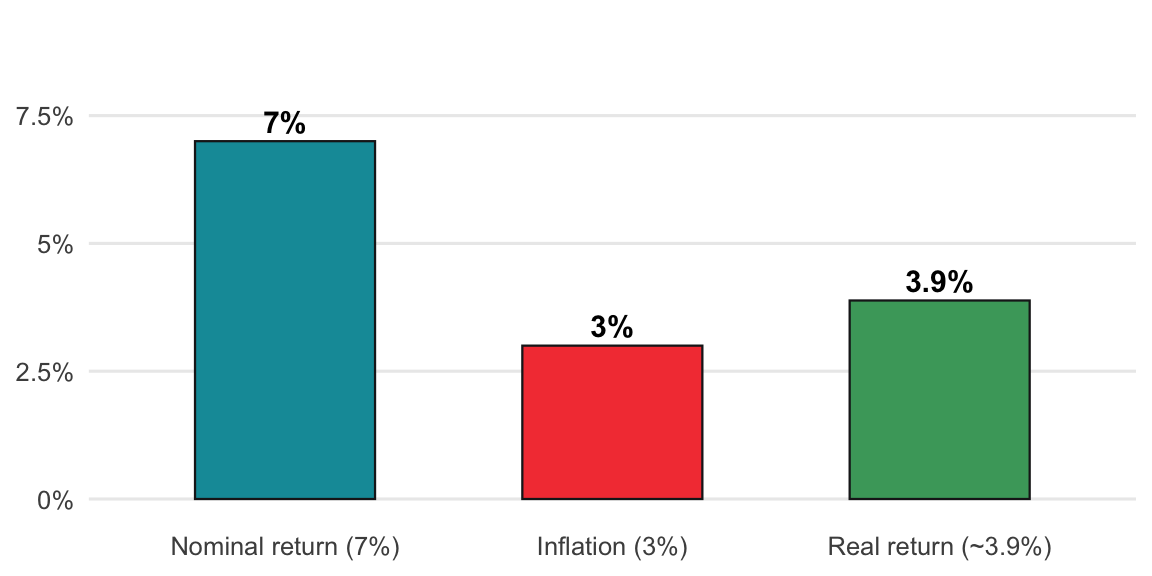

=FV(7%/12, 30*12, -500)4 Real (Inflation-Adjusted) Return

Nominal returns overstate purchasing power gains; inflation takes its slice every year.

Formula: Real Return = (1 + nominal) ÷ (1 + inflation) − 1

show/hide

real_return <- function(nominal, inflation) {

(1 + nominal) / (1 + inflation) - 1

}

real_return(nominal = 0.07, inflation = 0.03)

#> [1] 0.03883495show/hide

def real_return(nominal, inflation):

return (1 + nominal) / (1 + inflation) - 1

real_return(nominal=0.07, inflation=0.03)

#> 0.03883495145631066With nominal rate in A2 and inflation in B2:

=(1+A2)/(1+B2)-1