Major Purchases

1 Book Topics

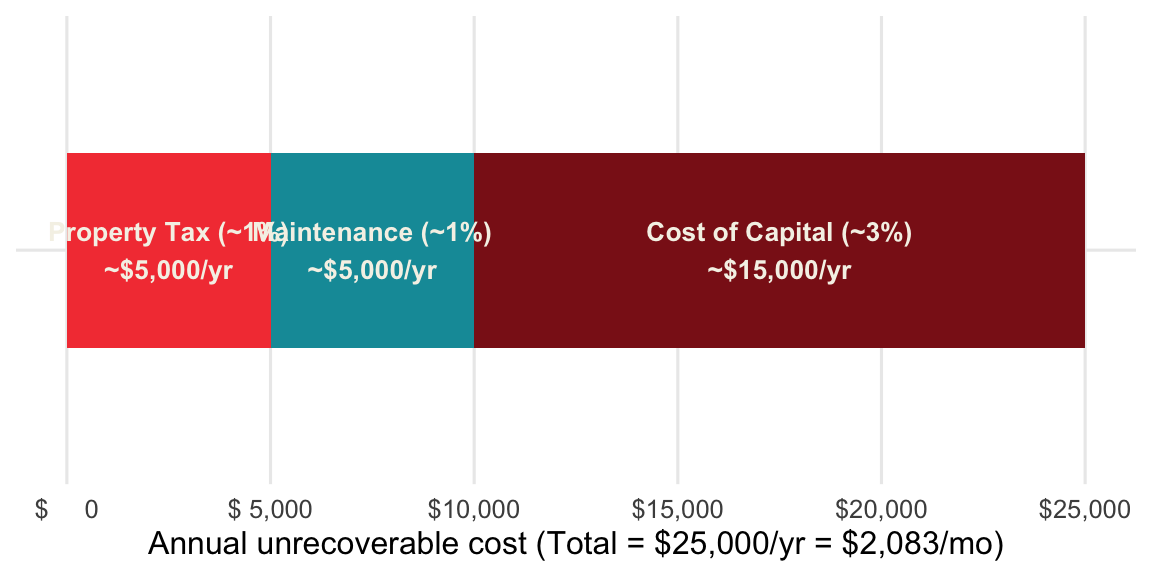

- Renting vs. buying: “renting is throwing money away” is a myth; unrecoverable costs of owning run ~5% of home value per year (Felix’s 5% Rule)

- 5% Rule components: property tax (~1%) + maintenance (~1%) + cost of capital (~3%) = ~5%/year; divide by 12 to get monthly equivalent

- When to buy: plan to stay 7+ years; stable income; won’t be “house poor” (housing <28–30% of gross income)

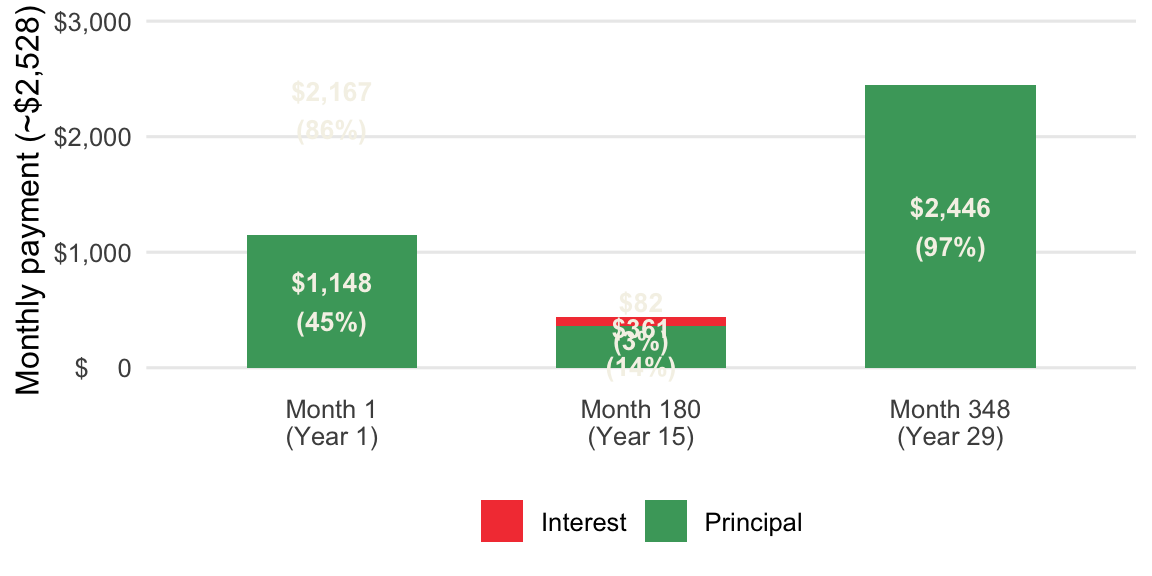

- Mortgage amortization: early payments are mostly interest (~75–80% in year 1 on a 30-year loan); moving every 5 years means you’ve barely touched principal

- Cars: depreciating assets; 20/4/10 rule (20% down, ≤4-year term, ≤10% gross income on transportation); buy used 2–4 years old

2 Rent vs. Buy Threshold (Felix’s 5% Rule)

Multiply home value by 5%, divide by 12. If you can rent an equivalent home for less, renting and investing the difference is likely the better financial choice.

Formula: Monthly ownership cost ≈ (Home Value × 0.05) ÷ 12

show/hide

rent_buy_threshold <- function(home_value, unrecoverable_rate = 0.05) {

(home_value * unrecoverable_rate) / 12

}

rent_buy_threshold(home_value = 600000)

#> [1] 2500show/hide

def rent_buy_threshold(home_value, unrecoverable_rate=0.05):

return (home_value * unrecoverable_rate) / 12

rent_buy_threshold(home_value=600000)

#> 2500.0With home value in A2:

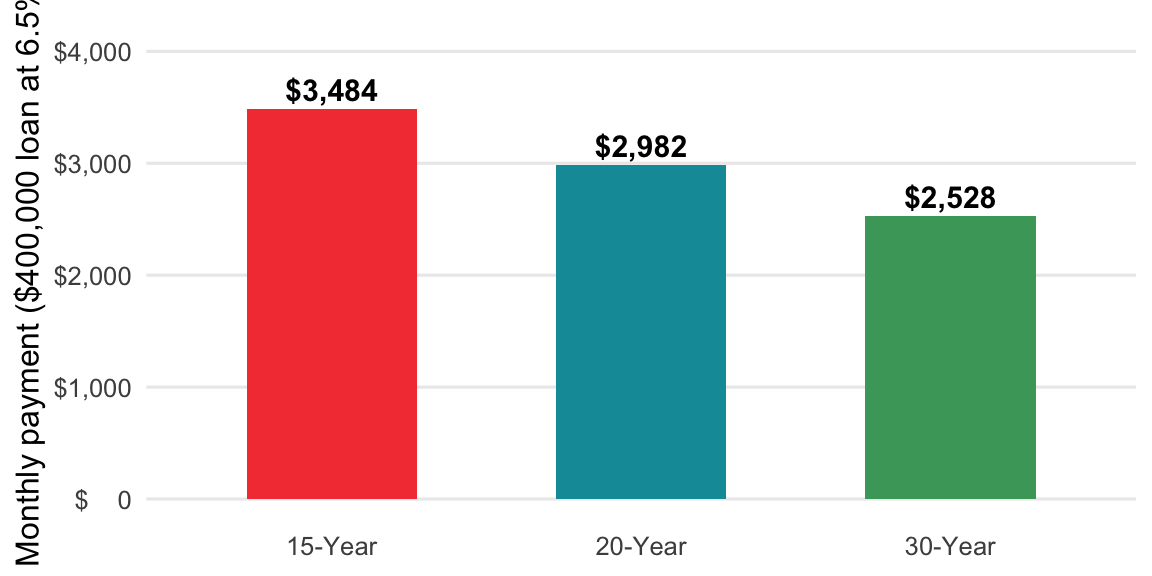

=(A2*0.05)/123 Monthly Mortgage Payment

The standard amortization formula; shorter terms mean higher payments but much less total interest.

Formula: M = P × [r(1 + r)^n] ÷ [(1 + r)^n − 1]

show/hide

mortgage_payment <- function(principal, annual_rate, years) {

r <- annual_rate / 12

n <- years * 12

principal * (r * (1 + r)^n) / ((1 + r)^n - 1)

}

# $480,000 loan at 6% over 30 years

mortgage_payment(principal = 480000, annual_rate = 0.06, years = 30)

#> [1] 2877.843show/hide

def mortgage_payment(principal, annual_rate, years):

r = annual_rate / 12

n = years * 12

return principal * (r * (1 + r) ** n) / ((1 + r) ** n - 1)

mortgage_payment(principal=480000, annual_rate=0.06, years=30)

#> 2877.8425207332334Use the built-in PMT() function: PMT(rate, nper, pv)

rate: monthly =6%/12nper: months =30*12pv: loan amount as negative =-480000

=PMT(6%/12, 30*12, -480000)4 First-Month Interest vs. Principal Split

Early mortgage payments are mostly interest; only the remainder reduces the balance.

Formulas:

- First-month interest = Principal × (annual rate ÷ 12)

- First-month principal = Monthly Payment − First-month interest

#> Warning: Removed 2 rows containing missing values or values outside

#> the scale range (`geom_col()`).

#> Warning: Removed 1 row containing missing values or values outside

#> the scale range (`geom_text()`).

show/hide

first_payment_split <- function(principal, annual_rate, years) {

payment <- mortgage_payment(principal, annual_rate, years)

interest <- principal * (annual_rate / 12)

data.frame(

payment = round(payment, 2),

interest = round(interest, 2),

principal = round(payment - interest, 2),

pct_interest = round((interest / payment) * 100, 1)

)

}

first_payment_split(principal = 480000, annual_rate = 0.06, years = 30)

#> # A tibble: 1 × 4

#> payment interest principal pct_interest

#> <dbl> <dbl> <dbl> <dbl>

#> 1 2878. 2400 478. 83.4show/hide

def first_payment_split(principal, annual_rate, years):

payment = mortgage_payment(principal, annual_rate, years)

interest = principal * (annual_rate / 12)

return {

"payment": round(payment, 2),

"interest": round(interest, 2),

"principal": round(payment - interest, 2),

"pct_interest": round((interest / payment) * 100, 1),

}

first_payment_split(principal=480000, annual_rate=0.06, years=30)

#> {'payment': 2877.84, 'interest': 2400.0, 'principal': 477.84, 'pct_interest': 83.4}With loan amount in A2, annual rate in B2, and monthly payment (from PMT()) in C2:

First-month interest:

=A2*(B2/12)First-month principal:

=C2-A2*(B2/12)