%%{init: {'theme': 'neutral', 'themeVariables': { 'fontFamily': 'monospace', "fontSize":"16px"}}}%%

flowchart TD

Crisis([Unexpected Expense]) --> NoFund{Emergency Fund?}

NoFund -->|No| CreditCard[Charge It to<br>Credit Card]

NoFund -->|Yes| EFund[Draw from<br>Emergency Fund]

CreditCard --> Interest[Pay 20-24% Interest<br>for Months/Years]

CreditCard --> Stress[Financial Stress<br>& Anxiety]

EFund --> Solved[Problem Solved<br>No Debt Added]

EFund --> Rebuild[Rebuild the Fund<br>Over Next Few Months]

style Crisis fill:#f0cfcf,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style NoFund fill:#f0cfcf,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style CreditCard fill:#f44242,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Interest fill:#f44242,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Stress fill:#f44242,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style EFund fill:#48a56a,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Solved fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style Rebuild fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

5 Emergency Fund

An emergency fund is cash set aside to handle the unexpected without reaching for credit. It’s the financial equivalent of a spare tire: you don’t need it most of the time, but when you do, nothing else will do the job.

The standard target is 3 to 6 months of essential expenses, parked somewhere safe and liquid. This chapter covers:

- How much you actually need

- Where to keep it (and where not to)

- How to build it from scratch

- How to rebuild it after a withdrawal

5.1 Why It Matters

Most financial derailments don’t start with bad investing. They start with a single unexpected expense — a car repair, a medical bill, a job loss — that gets charged to a credit card because there’s no cash available.

Housel’s framing is useful here: an emergency fund isn’t about the return on the money. It’s about buying options — the ability to not be forced into a bad financial decision at a bad time. That optionality is worth more than any interest rate .

5.2 How Much Do You Actually Need?

“3 to 6 months of expenses” is the standard answer, and it’s a reasonable starting range. But it isn’t a single number, because emergencies don’t affect everyone equally.

The Essential Expenses Baseline

Start by calculating your essential expenses — what it actually costs to keep the lights on. This is not your total spending; it’s the floor.

| Category | Examples |

|---|---|

| Housing | Rent or mortgage, renter’s/homeowner’s insurance |

| Food | Groceries (not dining out) |

| Utilities | Electricity, water, gas, internet |

| Transportation | Car payment, insurance, fuel, transit pass |

| Health | Insurance premiums, critical medications |

| Minimum debt payments | Credit card minimums, loan payments |

Entertainment, subscriptions, gym memberships, and dining out are not essential expenses for this calculation. In a true emergency, you can cut them. Your emergency fund is sized to cover the life you need, not the one you currently live.

Adjusting for Your Situation

The right target depends on how much income risk you carry. More risk = more months.

%%{init: {'theme': 'neutral', 'themeVariables': { 'fontFamily': 'monospace', "fontSize":"16px"}}}%%

flowchart TD

Start([How many months?]) --> Job{Job Stability?}

Job -->|Stable<br>single income| Dep{Dependents?}

Job -->|Variable / Self-Employed| More[Lean toward<br>6–9 months]

Dep -->|No| Insure{Good health &<br>disability coverage?}

Dep -->|Yes: kids, aging parents| SixPlus[6 months minimum]

Insure -->|Yes| ThreeToSix[3–4 months<br>is sufficient]

Insure -->|No| SixMonths[Closer to<br>6 months]

style Start fill:#48a56a,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Job fill:#f0cfcf,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style More fill:#f44242,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Dep fill:#f0cfcf,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style SixPlus fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Insure fill:#f0cfcf,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style ThreeToSix fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style SixMonths fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

A two-income household where both partners work stable salaried jobs has a lower emergency risk than a self-employed single parent. The fund should reflect that difference.

The Starter Fund First

Sethi’s approach is practical: build a $1,000 starter emergency fund immediately, even while paying down debt. Once high-interest debt is gone, shift the same monthly dollars you were paying toward debt into filling the emergency fund to its full target.

The sequence matters:

- Build $1,000 starter fund

- Eliminate credit card and high-interest debt (see Managing Debt)

- Build full 3–6 month fund

5.3 Emergency Reserves in the Financial Order of Operations

This sequence mirrors step 4 of Brian Preston’s Financial Order of Operations, introduced in Budgeting: emergency reserves are funded immediately after high-interest debt (step 3) and before Roth IRA/HSA contributions (step 5). See Managing Debt for how the two debt steps bracket this one.

Skipping ahead to invest before this step is funded exposes you to the exact sequencing risk described in Why Not the Stock Market? below — a market downturn and a job loss tend to arrive together.

5.4 Where to Keep It (and Where Not To)

An emergency fund has two jobs: stay safe and be available. This rules out most places you might initially consider.

%%{init: {'theme': 'neutral', 'themeVariables': { 'fontFamily': 'monospace', "fontSize":"16px"}}}%%

flowchart LR

Cash([Your Emergency<br>Fund]) --> Good["GOOD OPTIONS"]

Cash --> Bad["BAD OPTIONS"]

Good --> HYSA["High-Yield Savings Account<br>(HYSA)"]

Good --> MMF["Money Market Fund<br>(at a brokerage)"]

Good --> CheckFed["Federally Insured<br>Credit Union"]

Bad --> Checking["Regular Checking Account<br>(too easy to spend)"]

Bad --> Market["Stock Market<br>(too volatile)"]

Bad --> CD["Long-Term CDs<br>(penalties for early withdrawal)"]

Bad --> Cash2["Physical Cash at Home<br>(no interest, risk of loss)"]

style Cash fill:#48a56a,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Good fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Bad fill:#f44242,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style HYSA fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style MMF fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style CheckFed fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style Checking fill:#f44242,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Market fill:#f44242,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style CD fill:#f44242,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Cash2 fill:#f44242,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

The Right Account

A high-yield savings account (HYSA) at an FDIC-insured bank is the default recommendation. It earns meaningfully more than a standard checking account while keeping the money one business day away. Credit union equivalents covered by NCUA insurance work the same way.

See High-Yield Accounts for a full breakdown of how to find and open one.

Why Not the Stock Market?

This is the most common mistake people make with emergency funds. The logic seems sound: “my money would earn more in index funds.” The problem is sequencing risk.

If you lose your job in February and the stock market is down 25% at the same moment — which historically happens; recessions cause both — you’re forced to sell at the worst possible time. The emergency fund’s job isn’t to grow wealth; it’s to be there when you need it, at full value, on demand.

Ben Felix approaches this through the lens of human capital. For most, your ability to earn an income is your largest asset. An emergency fund is a hedge against the volatility of that human capital. If your income is highly variable (e.g., sales commissions, freelancing, or business ownership), you should lean toward a larger cash buffer to protect your ability to maintain your lifestyle during lean periods.

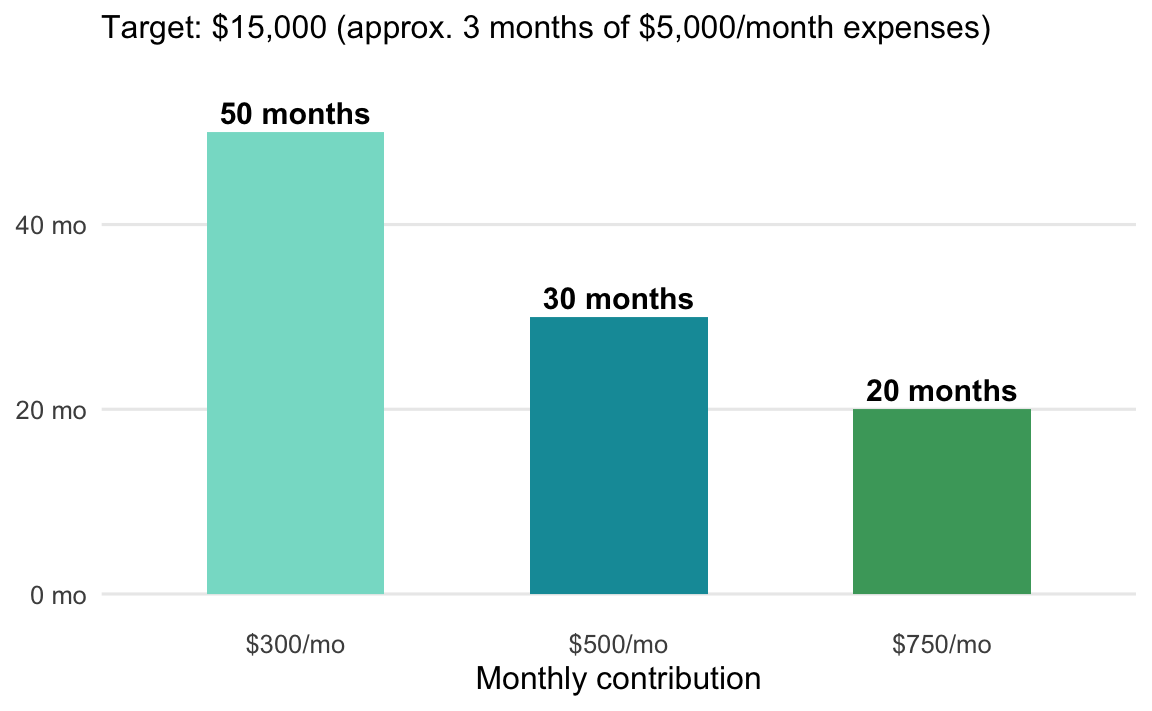

5.5 Building Your Emergency Fund

For most people, building the fund from zero to 3–6 months takes 12–24 months of consistent contribution. The chart below shows the monthly balance for three different monthly contribution amounts toward a $15,000 target.

The pattern is simple: doubling the monthly contribution roughly halves the time to goal.

Automate It

The most reliable way to build the fund is to treat it exactly like a bill. Set up an automatic transfer to your HYSA on payday, before you have a chance to spend the money. See Automating Savings for the full setup playbook.

Where to Find the Money

If you’re reading this and thinking “I don’t have anything extra to save,” the answer is usually a combination of small cuts applied consistently:

- Pause one subscription

- Cook at home one extra night per week

- Redirect a tax refund directly to the fund

None of these feel dramatic. That’s the point. The fund gets built one unexciting month at a time.

5.6 How to Rebuild After a Withdrawal

Using the emergency fund isn’t a failure — it’s the fund doing its job. The mistake is treating a withdrawal as a one-time event rather than a signal to rebuild immediately.

%%{init: {'theme': 'neutral', 'themeVariables': { 'fontFamily': 'monospace', "fontSize":"16px"}}}%%

flowchart TD

Use([Emergency: Fund Used]) --> Assess[Assess: How much<br>was withdrawn?]

Assess --> Resume[Resume automatic<br>contributions immediately]

Resume --> Temp{Can you temporarily<br>increase contributions?}

Temp -->|Yes| Boost[Increase monthly<br>contribution until rebuilt]

Temp -->|No| Steady[Maintain existing<br>contribution; stay patient]

Boost --> Target([Fund Restored])

Steady --> Target

style Use fill:#f0cfcf,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style Assess fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Resume fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Temp fill:#f0cfcf,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style Boost fill:#48a56a,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Steady fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style Target fill:#48a56a,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

Two rules for the rebuild phase:

Don’t stop other savings to rebuild faster. The automatic contributions will get you there. Don’t interrupt retirement account contributions, especially if you have an employer match.

Don’t restart debt payoff conversations during the rebuild. Your priority order right now is: minimum payments on everything, then rebuild the emergency fund, then return to accelerated debt payoff.

5.7 Math for Emergency Funds

The calculations here are simple, but writing them down forces you to confront the actual numbers.

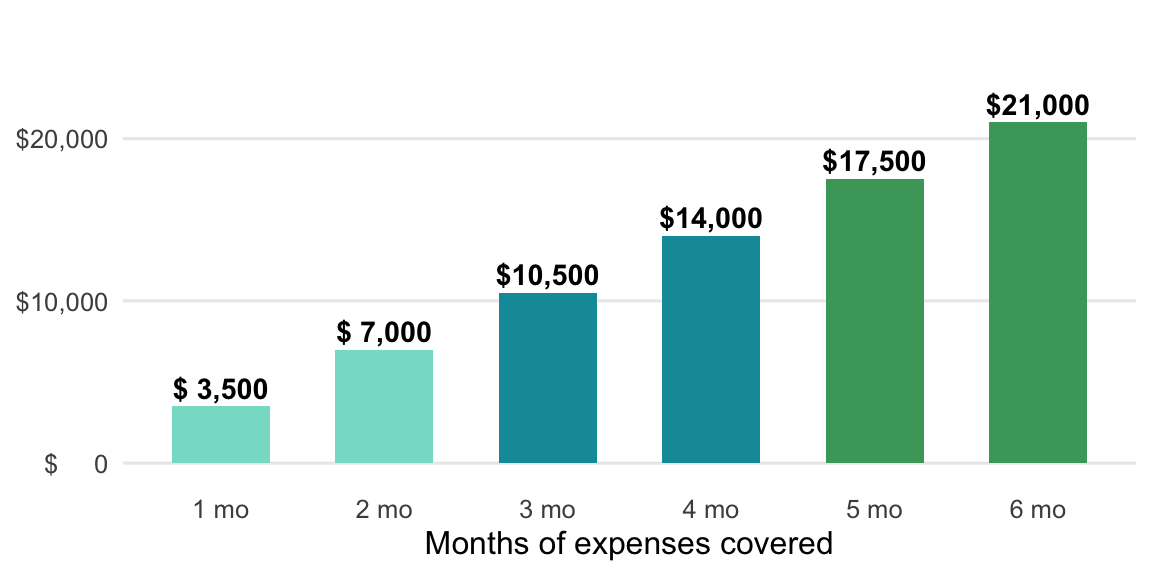

Your Target Amount

Your emergency fund target is just essential monthly expenses multiplied by the number of months you want to cover.

The chart below shows how the target grows as you add months — each bar is the previous one plus one more month of expenses.

Formula: Target = Monthly Essential Expenses × Months of Coverage

Example: $3,500/month in essential expenses × 4 months = $14,000 target.

show/hide

emergency_fund_target <- function(monthly_expenses, months = 3) {

monthly_expenses * months

}

# $3,500/month in essential expenses, 3-month and 6-month targets

emergency_fund_target(monthly_expenses = 3500, months = 3)

#> [1] 10500

emergency_fund_target(monthly_expenses = 3500, months = 6)

#> [1] 21000show/hide

def emergency_fund_target(monthly_expenses, months=3):

return monthly_expenses * months

# $3,500/month in essential expenses, 3-month and 6-month targets

print(emergency_fund_target(monthly_expenses=3500, months=3))

#> 10500

print(emergency_fund_target(monthly_expenses=3500, months=6))

#> 21000Months to Reach Your Target

Given your current balance and a monthly contribution, how long until you reach the target?

Formula: Months to Goal = (Target − Current Balance) ÷ Monthly Contribution

Example: $14,000 target, $2,000 already saved, contributing $500/month → (14,000 − 2,000) ÷ 500 = 24 months.

show/hide

months_to_ef_goal <- function(target, current_balance, monthly_contribution) {

remaining <- max(0, target - current_balance)

ceiling(remaining / monthly_contribution)

}

# $14,000 target, $2,000 saved, $500/month contribution

months_to_ef_goal(target = 14000, current_balance = 2000, monthly_contribution = 500)

#> [1] 24show/hide

import math

def months_to_ef_goal(target, current_balance, monthly_contribution):

remaining = max(0, target - current_balance)

return math.ceil(remaining / monthly_contribution)

# $14,000 target, $2,000 saved, $500/month contribution

print(months_to_ef_goal(target=14000, current_balance=2000, monthly_contribution=500))

#> 24Contribution Needed by a Deadline

Working backwards: if you want to reach your target in a specific number of months, how much do you need to save each month?

Formula: Monthly Contribution = (Target − Current Balance) ÷ Months Remaining

Example: You want a full $14,000 fund in 18 months and have $2,000 now → (14,000 − 2,000) ÷ 18 = $667/month.

show/hide

monthly_contribution_needed <- function(target, current_balance, months) {

remaining <- max(0, target - current_balance)

ceiling(remaining / months)

}

# $14,000 target, $2,000 saved, want to finish in 18 months

monthly_contribution_needed(target = 14000, current_balance = 2000, months = 18)

#> [1] 667show/hide

def monthly_contribution_needed(target, current_balance, months):

remaining = max(0, target - current_balance)

return math.ceil(remaining / months)

# $14,000 target, $2,000 saved, want to finish in 18 months

print(monthly_contribution_needed(target=14000, current_balance=2000, months=18))

#> 667What the Fund Earns While You Build It

Keeping the fund in a HYSA means it earns interest as it grows. This won’t dramatically change your timeline, but it’s real money.

Formula: Future Value = Balance × (1 + monthly rate)^months

Where monthly rate = annual rate ÷ 12.

Example: $14,000 in a HYSA at 4.5% APY, untouched for 12 months → ~$14,630. The interest pays for a car repair without reducing your fund.

show/hide

ef_growth <- function(balance, annual_rate, months) {

monthly_rate <- annual_rate / 12

balance * (1 + monthly_rate)^months

}

# $14,000 at 4.5% APY for 12 months

ef_growth(balance = 14000, annual_rate = 0.045, months = 12)

#> [1] 14643.16show/hide

def ef_growth(balance, annual_rate, months):

monthly_rate = annual_rate / 12

return balance * (1 + monthly_rate) ** months

# $14,000 at 4.5% APY for 12 months

print(ef_growth(balance=14000, annual_rate=0.045, months=12))

#> 14643.1575505682545.8 Putting It All Together

%%{init: {'theme': 'neutral', 'themeVariables': { 'fontFamily': 'monospace', "fontSize":"16px"}}}%%

flowchart TD

Start(["Build Your<br>Emergency Fund"]) --> Step1("Step 1. Calculate monthly<br>essential expenses")

Step1 --> Step2("Step 2. Choose your target:<br>3–6 months, based on risk")

Step2 --> Step3("Step 3. Open a<br>dedicated HYSA")

Step3 --> Step4("Step 4. Set up automatic<br>monthly transfer on payday")

Step4 --> Step5("Step 5. Build $1,000 starter<br>fund first if in debt")

Step5 --> Step6("Step 6. Pay off high-interest<br>debt, then fill full fund")

Step6 --> Step7("Step 7. Once funded, leave it<br>alone — it's not savings")

Step7 --> Step8(["Step 8. Rebuild immediately<br>after any withdrawal"])

style Start fill:#48a56a,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Step1 fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Step2 fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Step3 fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Step4 fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Step5 fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Step6 fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Step7 fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Step8 fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

5.9 Key takeaways

An emergency fund is not an investment. It’s insurance — and the cost of that insurance is the interest you don’t earn by keeping it in cash instead of equities. That’s a reasonable price for what it buys.

- Size it to your actual risk. Stable salaried job with good coverage? Three months is fine. Variable income or dependents? Six months or more.

- Keep it separate. A dedicated HYSA with a slight friction to transfer prevents casual spending from eroding the fund.

- Build it in stages. $1,000 starter fund first, then full fund after high-interest debt is cleared.

- Automate the contribution. Set it on payday and treat it like a bill until the fund is full.

- Rebuild immediately after using it. The fund only works if it’s there the next time you need it.

As Housel writes, the point of financial margin isn’t to optimize — it’s to survive. An emergency fund doesn’t make you rich. It keeps a bad month from becoming a bad decade.