%%{init: {'theme': 'neutral', 'themeVariables': { 'fontFamily': 'monospace', "fontSize":"16px"}}}%%

flowchart TD

TotalWealth(["Your Total<br>Economic Wealth"]) --> HumanCapital("Human Capital:<br/>Future Earning Potential")

TotalWealth --> FinancialCapital("Financial Capital:<br/>Investments & Savings")

HumanCapital --> EarlyCareer("Early Career:<br/>Human Capital is HUGE")

FinancialCapital --> EarlyCareer2("Early Career:<br/>Financial Capital is small")

EarlyCareer --> Implication["Implication:<br>Invest in Skills,<br/>Education &<br>Career Growth"]

EarlyCareer2 --> Implication2[Implication:<br>Take More Equity<br>Risk When Young]

style TotalWealth fill:#48a56a,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style HumanCapital fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style FinancialCapital fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style EarlyCareer fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style EarlyCareer2 fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Implication fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style Implication2 fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

1 Income

Building wealth doesn’t start with picking the right stock or finding a hot investment; it starts with how you manage the money flowing in and out of your life. Let’s break down the foundational principles.

1.1 Some Core Truths

Here’s a counterintuitive insight from Morgan Housel1:

“Wealth is the nice cars not purchased. The diamonds not bought. The watches not worn, the clothes forgone and the first-class upgrade declined. Wealth is financial assets that haven’t yet been converted into the stuff you see.” - Morgan Housel

The person driving the flashy car isn’t necessarily wealthy; they just spent their money on a car. True wealth is the income you didn’t spend, quietly compounding in the background.

Ben Felix reinforces this with hard data. Research consistently shows that conspicuous consumption (signaling wealth through purchases) is negatively correlated with actual wealth.2 People who look rich usually aren’t, while the people who are rich typically live below their income level.

1.2 Your Human Capital

One of Felix’s most powerful contributions is reframing how we think about income itself. He encourages investors to view themselves as having two forms of capital. When you’re young, your single biggest asset is your future earning potential.

During this time, investing in skills, education, and career mobility will have a higher return than any portfolio decision. Income growth, especially early in your career, is one of the most powerful wealth-building levers available. Time and energy spent developing valuable skills can pay off in later years (when these resources are less readily available).

1.3 Spending and Happiness

The academic research on money and well-being tends to show some practical conclusions:

- Experiences beat possessions. Research shows experiential purchases generate more lasting happiness than material ones.3 Choose a vacation or night out over new clothes or toys.

- Buying time is one of the highest-return uses of money. Outsourcing tasks you dislike (cleaning, lawn care, commuting time) correlates strongly with life satisfaction.4 Real wealth should be measured in not doing things you don’t like to do (and more time spent doing things you like to do).

- Lifestyle inflation is the silent killer. Hedonic adaptation means each lifestyle upgrade quickly becomes the new baseline, but the financial commitment remains permanent.5 This is the classic “keeping up with the Jonses” trap: avoid external comparisons of material wealth. Instead, focus on where you were last year (and where you’d like to be in the next year).

- Housing is the biggest lever. Housing is usually your biggest expense, so choosing how much to spend on it greatly affects your wealth. Renting can be as good as (or better than) buying when you crunch the numbers.6

1.4 Three Anchoring Rules

1. Sethi: “Spend on What You Love, Cut on What You Don’t”

Love coffee? Buy the $6 latte. But maybe drive a reliable used car instead of a luxury lease. The goal isn’t deprivation; it’s intentionality.7

2. Housel: “Build a Gap Between Ego and Income”

The wider the gap between what you earn and what your ego demands you spend, the wealthier you become. Lifestyle creep is the silent killer of financial freedom.8

3. Bogle: “Keep It Simple”

Bogle’s philosophy applies to spending, too: complexity is the enemy. The more complicated your financial life, the easier it is to lose track. Automate, simplify, repeat.9

1.5 Wealth vs Income

Scott Galloway, an NYU Stern professor and host of the Prof G podcasts, distills the whole problem into a single equation in his 2024 book The Algebra of Wealth:10

The Wealth Formula:

Wealth = Focus + (Stoicism × Time × Diversification)

The four variables are the four levers you actually control:

Focus: pick something economically valuable and become great at it. Career, geography, and skill choice compound harder than any single financial decision early on. This is Galloway’s version of Felix’s human capital; your earning engine is the asset you build first.

Stoicism: your willingness to live below your means without needing to signal otherwise will keep you from spending money you don’t have on things you don’t really need. Galloway, Housel, and Sethi all agree here; spending discipline is a character trait before it’s a budget.11

Time: The most powerful financial variable is how many compounding years you still have. The earlier you start, the more time you have.

Diversification: Don’t bet on a single stock, sector, or career outcome. Spread risk across asset classes, geographies, and time.

%%{init: {'theme': 'neutral', 'themeVariables': { 'fontFamily': 'monospace', "fontSize":"16px"}}}%%

flowchart TD

Wealth(["<strong>Wealth</strong>"]) --> Focus("Focus is <br><em>ADDITIVE</em>")

Wealth --> SecondTerm("Second term is<br/><em>MULTIPLICATIVE</em><br>")

SecondTerm --> Stoicism("<strong>STOICISM</strong><br>Living Below Means")

SecondTerm --> Time("<strong>TIME</strong><br>Years Compounding")

SecondTerm --> Diversification("<strong>DIVERSIFICATION</strong><br>Smart Allocation")

Focus -.Standalone Contribution.-> SomeWealth(["<strong>FOCUS</strong><br>builds some wealth<br>even if others<br>fail"])

Stoicism --> Multiply{"Multiply<br>Together"}

Time --> Multiply

Diversification --> Multiply

Multiply --> Compounding(["<strong>Compounding<br>Wealth Engine</strong>"])

style Wealth fill:#48a56a,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style SecondTerm fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Stoicism fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Time fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Diversification fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Focus fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Compounding fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style SomeWealth fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style Multiply fill:#f0cfcf,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

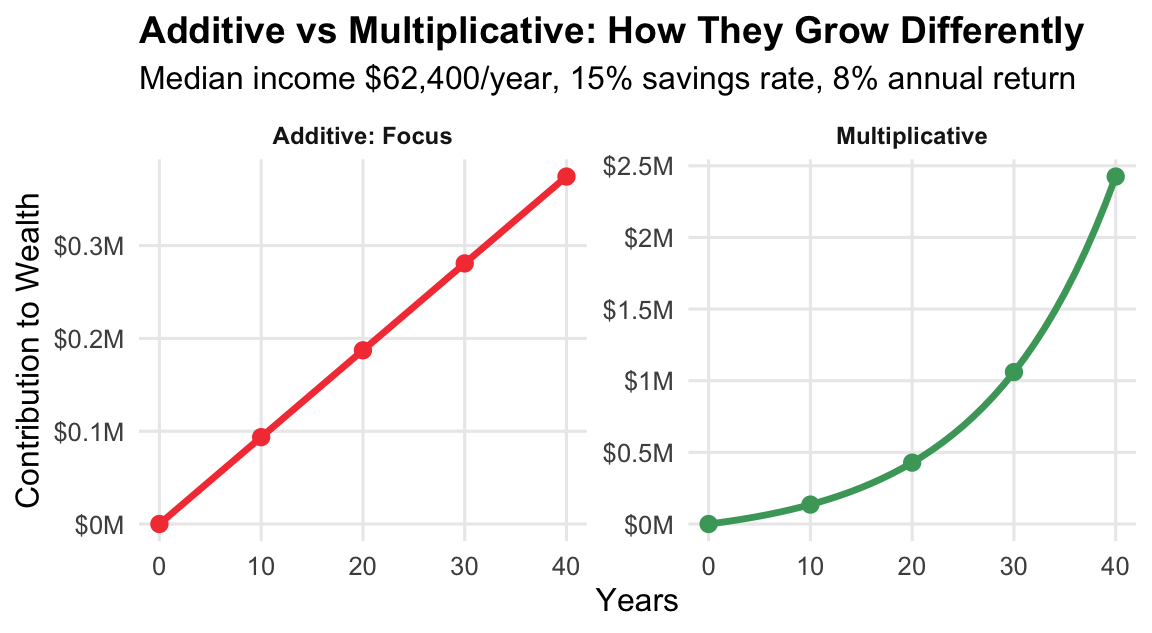

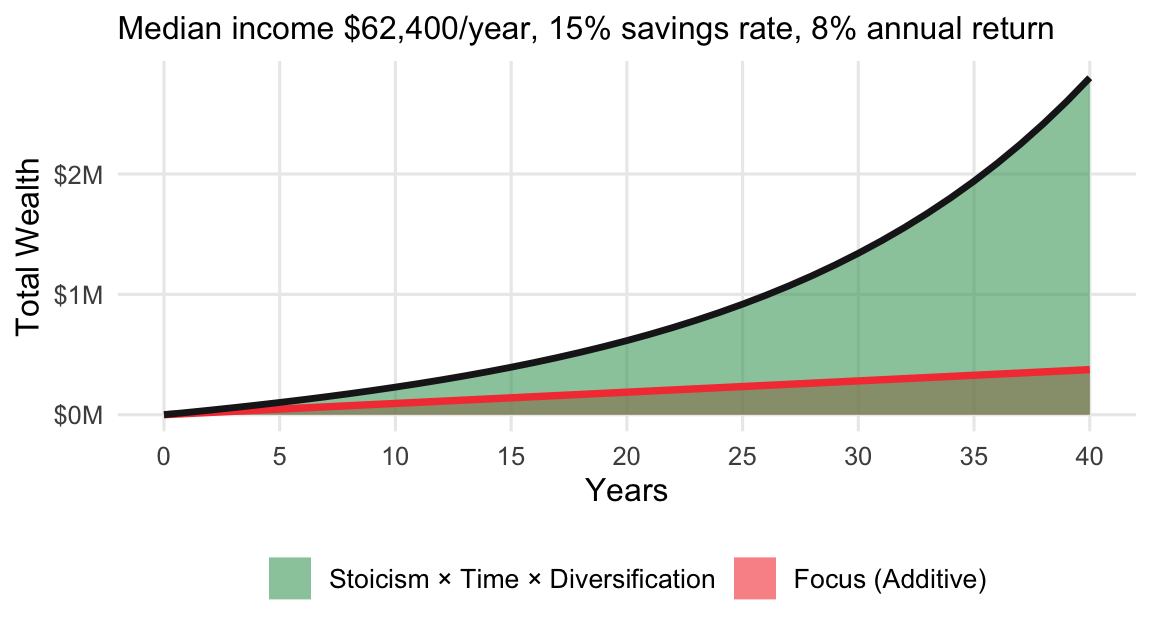

The arithmetic does a lot of the teaching on its own. Focus is additive, which means even with poor execution on the other three, a strong income engine still builds some wealth.

However, stoicism, time, and diversification are multiplicative, so a zero on any one of these collapses the whole second term. In plain language: spending above your means (i.e., saving and investing nothing) for forty years compounds to nothing.

The chart below illustrates this arithmetic.

Focus contributes in a straight line (additive), while stoicism, time, and diversification compound exponentially.

After 40 years, the multiplicative term dominates the total.

The illustration uses concrete assumptions: median income of $62,400, saving 15% yearly ($9,360, stoicism), and earning 8% annually (diversification). The red area grows linearly. The green area curves upward, eventually dwarfing the red. This is the power of compound growth.

1.6 As Your Income Grows

This is where most people fail. A raise feels like permission to upgrade everything. Instead, focus on Felix’s research-backed advice: the marginal happiness gained from lifestyle upgrades is much smaller than people expect, while the marginal financial security from saving raises is enormous.

%%{init: {'theme': 'neutral', 'themeVariables': { 'fontFamily': 'monospace', "fontSize":"16px"}}}%%

flowchart TD

Raise(["Pay Raise"]) --> Split{"<strong>Split the Raise</strong>"}

Split --> HalfInvest["50% to<br>Investing/Savings"]

Split --> HalfLifestyle["50% to<br>Lifestyle"]

HalfInvest --> WealthGrows(["Wealth Compounds"])

HalfLifestyle --> EnjoyNow(["Enjoy the Win"])

style Raise fill:#48a56a,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style Split fill:#f0cfcf,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style HalfInvest fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style HalfLifestyle fill:#0e9aa7,color:#F5F2E8,stroke:#1C1C1E,stroke-width:2px

style WealthGrows fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

style EnjoyNow fill:#86ddcd,color:#1C1C1E,stroke:#1C1C1E,stroke-width:2px

browser() or breakpointThis way, you reward yourself and accelerate freedom, without falling into the trap of inflating your lifestyle to match every dollar.

1.7 Math for Income

This chapter is mostly about behavior, but I’ll cover some numbers below that can turn the behaviors into something you can track. Each calculation below is also written as an R and Python function, which are covered in the callout box below.

NoteR vs Python: assignment and functions

The first two differences you’ll see between R and Python in this book are how each language names things and how each language defines functions.

Assignment

R uses <- by convention (= also works).

Python uses =.

x <- 10x = 10Function definition

R uses function() and assigns the result to a name. The body is wrapped in curly braces {}.

Python uses the def keyword, followed by a colon and an indented body.

add_fun <- function(a, b) {

a + b

}def add_fun(a, b):

return a + bThe Wealth Formula

Galloway’s wealth formula captures the essence of wealth building:

Formula: Wealth = Focus + (Stoicism × Time × Diversification)

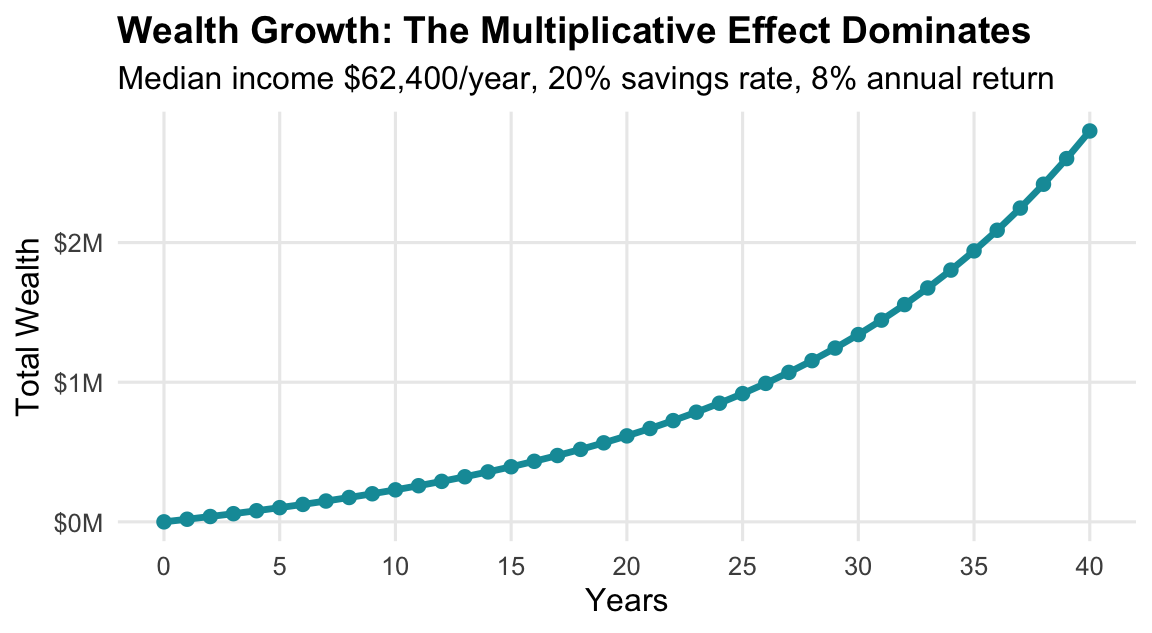

Example: median income $62,400, saving 15% ($9,360/year), earning 8% annually over 40 years.

show/hide

wealth_formula <- function(median_income, savings_rate, annual_return, years) {

# annual savings contribution over time (additive)

focus <- (median_income * savings_rate) * years

# compound growth of savings (multiplicative)

annual_savings <- median_income * savings_rate

multiplicative <- annual_savings * (((1 + annual_return)^years - 1) / annual_return)

# wealth

focus + multiplicative

}After 40 years with median income, 15% savings rate, 8% return:

show/hide

wealth_formula(

median_income = 62400,

savings_rate = 0.15,

annual_return = 0.08,

years = 40

)

#> [1] 2799169show/hide

def wealth_formula(median_income, savings_rate, annual_return, years):

# annual savings contribution over time (additive)

focus = (median_income * savings_rate) * years

# compound growth of savings (multiplicative)

annual_savings = median_income * savings_rate

multiplicative = annual_savings * (((1 + annual_return)**years - 1) / annual_return)

# wealth

return focus + multiplicativeAfter 40 years with median income, 15% savings rate, 8% return:

show/hide

wealth_formula(

median_income=62400,

savings_rate=0.15,

annual_return=0.08,

years=40

)

#> 2799169.0151255885In Excel, we can break this into two columns for clarity. Let’s say we have:

A2: median income ($62,400)

B2: savings rate (0.15)

C2: annual return (0.08)

D2: years (40)

For the focus (additive) component in cell E2:

=A2*B2*D2For the multiplicative component in cell F2:

=(A2*B2)*(((1+C2)^D2-1)/C2)For total wealth in G2:

=E2+F2

The result is approximately $2.8 million after 40 years—a powerful demonstration of how modest, consistent saving paired with compound growth transforms modest income into substantial wealth.

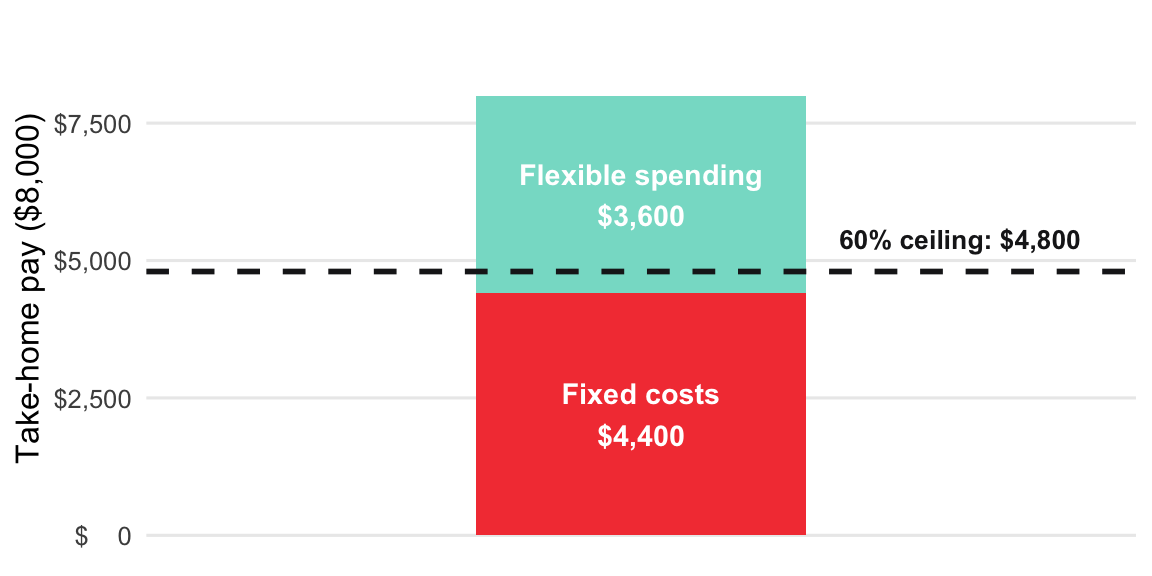

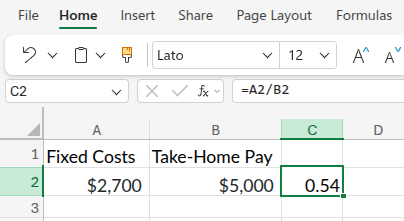

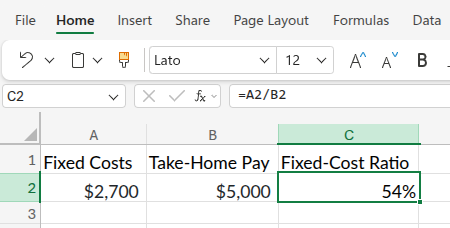

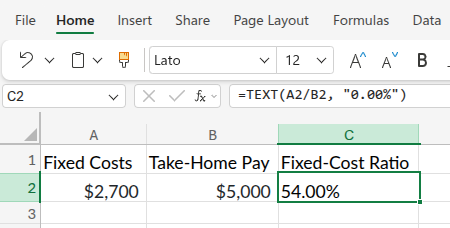

The Fixed-Cost Ratio

Fixed costs (rent, loan payments, insurance, utilities) are the commitments you can’t easily change month to month. The chart below divides an $8,000 take-home into its two parts — fixed and flexible — and marks the 60% ceiling that keeps the rest of the budget healthy.

The formula names the fixed slice as a fraction of the whole bar, converted to a percentage.

Formula: Fixed-Cost Ratio = Fixed Costs ÷ Take-Home Pay × 100

Example: $4,400 of fixed costs on $8,000 take-home

Below is an implementation of this function in R:

show/hide

fixed_cost_ratio <- function(fixed_costs, take_home) {

(fixed_costs / take_home) * 100

}$4,400 of fixed costs on $8,000 take-home pay

show/hide

fixed_cost_ratio(fixed_costs = 4400, take_home = 8000)

#> [1] 55The same formula in Python:

show/hide

def fixed_cost_ratio(fixed_costs, take_home):

return (fixed_costs / take_home) * 100$4,400 of fixed costs on $8,000 take-home pay

show/hide

fixed_cost_ratio(fixed_costs=4400, take_home=8000)

#> [1] 55In Excel there’s no function to define: you put the numbers in cells and write the formula once. Enter the fixed costs in cell A2 and take-home pay in B2, then in C2:

=A2/B2That gives 0.54.

Format C2 as a percentage (Home → %, or Ctrl+Shift+5) and it displays 54%.

To produce the percent string directly (the analog of R’s paste0(..., "%") and Python’s f-string), use TEXT() instead:

=TEXT(A2/B2, "0.0%")

TEXTThis results in a 55% fixed-cost ratio – just under the ceiling!

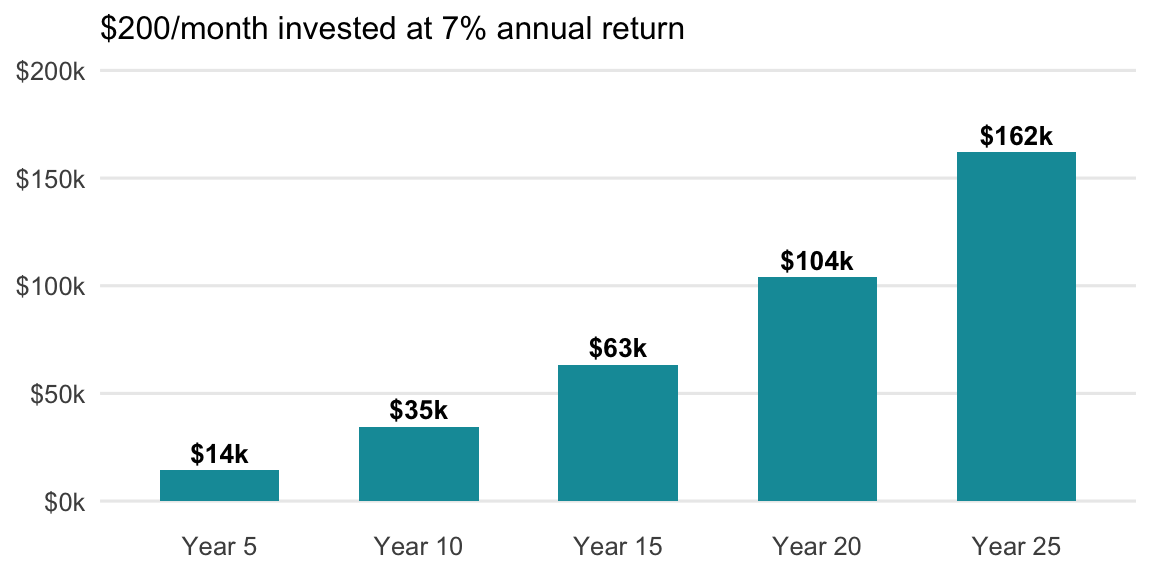

What a Raise Is Really Worth

$200/month doesn’t sound like much. The chart below shows what that single habit produces when invested at 7% over 25 years.

Each bar is the previous total plus another year of $200/month contributions and their growth — the annuity formula sums all those monthly additions into one calculation.

Formula: FV = PMT × [((1 + r)^n − 1) ÷ r]

PMT is the amount invested each month, r is the monthly return, and n is the number of months. We will revisit this future-value-of-contributions formula in the Investing Basics chapter.

Example: a $400/month raise, half of it invested ($200/month) for 25 years at a 7% annual return.

Here is an example of this function in R:

show/hide

raise_invested_value <- function(monthly_raise, invest_share, rate, years) {

contribution <- monthly_raise * invest_share

monthly_rate <- rate / 12

periods <- years * 12

contribution * (((1 + monthly_rate)^periods - 1) / monthly_rate)

}Half of a $400/month raise, invested for 25 years at 7%

show/hide

raise_invested_value(

monthly_raise = 400,

invest_share = 0.5,

rate = 0.07,

years = 25)

#> [1] 162014.3Below is the same function in Python:

show/hide

def raise_invested_value(monthly_raise, invest_share, rate, years):

contribution = monthly_raise * invest_share

monthly_rate = rate / 12

periods = years * 12

return contribution * (((1 + monthly_rate) ** periods - 1) / monthly_rate)Half of a $400/month raise, invested for 25 years at 7%

show/hide

raise_invested_value(monthly_raise=400, invest_share=0.5, rate=0.07, years=25)

#> 162014.33860462217Excel actually has a built-in FV() (future value) function, so we don’t have to write the formula ourselves. The arguments are FV(rate, nper, pmt):

rateis the return per period (monthly here):7%/12

nperis the number of periods:25*12

pmtis the amount invested each period, entered as a negative number because it’s cash leaving your pocket:-200

=FV(7%/12, 25*12, -200)

This returns $162,014.34, the same result as the R and Python functions above. (Excel reports a positive number because the contributions were entered as negative cash flows.)

We can see this results in over $160K!

1.8 Key takeaways

Invest in your human capital: your career is your biggest asset early on and it’s the focus part of the wealth equation.

Track your fixed costs: aim to keep them under 60% of your take-home pay. Stoicism aligns with Housel’s “gap between ego and income.” Living within your means isn’t about restriction; it’s about control and intention.

Spend the rest without guilt on what genuinely brings you joy: prioritize experiences and time over possessions. As Housel puts it, the highest form of wealth is the ability to wake up and say, “I can do whatever I want today.”

Keep it simple: Bogle’s philosophy is diversification at the portfolio level, and time is on the side of the compounding effect (which we will return to in Investing).

Wealth is a combination of growing your income, protecting your savings, and making sure you’re spending money on what actually makes you happy.

Read more in Morgan Housel’s The Psychology of Money↩︎

Read more in Social class, social self-esteem, and conspicuous consumption.↩︎

Van Boven, L., & Gilovich, T. (2003). “To do or to have? That is the question.” Journal of Personality and Social Psychology, 85(6), 1193–1202. https://doi.org/10.1037/0022-3514.85.6.1193↩︎

Whillans, A. V., Dunn, E. W., Smeets, P., Bekkers, R., & Norton, M. I. (2017). “Buying time promotes happiness.” Proceedings of the National Academy of Sciences, 114(32), 8523–8527. https://doi.org/10.1073/pnas.1706541114↩︎

Dunn, E. W., Gilbert, D. T., & Wilson, T. D. (2011). “If money doesn’t make you happy, then you probably aren’t spending it right.” Journal of Consumer Psychology, 21(2), 115–125. https://doi.org/10.1016/j.jcps.2011.02.002↩︎

Beracha, E., & Johnson, K. H. (2012). “Lessons from over 30 years of buy versus rent decisions: Is the American dream always wise?” Real Estate Economics, 40(2), 217–247. https://doi.org/10.1111/j.1540-6229.2011.00321.x. See also Ben Felix’s analysis at PWL Capital and the Rational Reminder podcast.↩︎

Sethi, R. (2019). I Will Teach You to Be Rich (2nd ed.). Workman Publishing. The phrase “spend extravagantly on the things you love, and cut costs mercilessly on the things you don’t” is the core of Sethi’s “Conscious Spending Plan” (see Chapter 4, Conscious Spending). More at https://www.iwillteachyoutoberich.com/.↩︎

Housel, M. (2020). The Psychology of Money: Timeless lessons on wealth, greed, and happiness. Harriman House. The “gap between your ego and your income” framing appears in Chapter 10, Save Money. The chapter draws on Housel’s earlier essay of the same name at Collaborative Fund.↩︎

Bogle, J. C. (2017). The Little Book of Common Sense Investing: The Only Way to Guarantee Your Fair Share of Stock Market Returns (10th Anniversary ed.). Wiley. Bogle’s recurring mantra (“Simplicity is the master key to financial success”) runs throughout the book and his earlier Common Sense on Mutual Funds. The investor community he inspired distills these ideas at https://www.bogleheads.org/wiki/Bogleheads%C2%AE_investment_philosophy.↩︎

Galloway, S. (2024). The Algebra of Wealth: A Simple Formula for Financial Security. Portfolio (Penguin Random House). See profgalloway.com for his writing, podcasts, and the weekly No Mercy / No Malice newsletter.↩︎